EIC Predicts BoT to Maintain Policy Rate Throughout 2021 Despite Significant Economic Slowdown from COVID-19 Wave 3

EIC Predicts BoT to Maintain Policy Rate Throughout 2021 Despite Significant Economic Slowdown from COVID-19 Wave 3

· The BoT unanimously decided to maintain the policy interest rate at 0.5% per annum, despite assessing that the Thai economy is likely to slow down significantly due to the COVID-19 outbreak in its third wave, as the BoT views that the most critical challenge for the Thai economy is the procurement and distribution of vaccines in a timely and sufficient manner.

· The BoT assessed that credit measures and accelerating debt restructuring will more effectively alleviate financial burdens than further reducing the already low policy interest rate.

· The financial situation in Thailand has eased in some aspects, as the yield on Thai government bonds has decreased in line with the decline in U.S. government bond yields, and the Thai baht has weakened against competing currencies. However, the distribution of liquidity remains uneven, particularly among SMEs due to increased credit risks.

EIC expects the BoT to maintain the policy interest rate at 0.5% throughout 2021 and to focus more on enhancing the efficiency of monetary policy to distribute liquidity to affected businesses, emphasizing support for debt restructuring, and may extend the period for reducing contributions to the Financial Institutions Development Fund (FIDF).

Key points

The BoT unanimously decided to maintain the policy interest rate at 0.5% per annum and assessed that the Thai economy is likely to slow down significantly due to the third wave of the outbreak. In the Monetary Policy Committee meeting on May 5, 2021, the BoT unanimously decided to maintain the policy interest rate at 0.5% per annum, as the committee views that the most critical challenge for the Thai economy is the timely and sufficient procurement and distribution of vaccines. The key financial measures are to distribute liquidity to businesses and households affected by the new outbreak, particularly credit measures and accelerating debt restructuring, which will more effectively alleviate financial burdens than reducing the policy interest rate. Therefore, it is deemed appropriate to maintain the policy interest rate and preserve the limited capacity for monetary policy implementation.

- The Thai economy is likely to slow down due to the third wave of the outbreak, which impacts domestic spending and the recovery of foreign tourists due to slower-than-expected reopening and uncertain international travel policies. The main driver of the Thai economy comes from the recovery of exports in line with the economies of trading partners, but the positive effects on overall labor market employment remain limited. Meanwhile, government relief measures and additional financial measures will support the short-term recovery of the economy, but government stimulus in fiscal year 2022 may decrease due to accelerated disbursement of the current fiscal year borrowing bill.

- General inflation is expected to temporarily rise in the second quarter of 2021 due to low crude oil prices in the same quarter of the previous year, while medium-term inflation forecasts remain anchored within target ranges.

- Key risks for the Thai economy in the near future include (1) the distribution and effectiveness of COVID-19 vaccines, (2) uneven recovery leading to increased labor market vulnerability affecting household income and private consumption, and (3) additional financial fragility, particularly among SMEs and tourism businesses, which have reduced debt repayment capacity due to declining income, while households have a lower savings-to-income ratio, reducing their ability to cover expenses.

According to the BoT's assessment, if the government can procure and distribute an additional 100 million vaccine doses in 2021, it will result in a 2% GDP growth for Thailand in 2021 and 4.7% in 2022 (not including any additional government measures). However, in a worst-case scenario, if the government procures and distributes vaccines slower than the original plan, it will result in only 1% GDP growth in 2021 and 1.1% in 2022.

- If the government can distribute vaccines according to the target of 100 million doses in 2021, it will result in a 2% GDP growth in 2021 and 4.7% in 2022, with 1.2 million and 15 million foreign tourists in 2021 and 2022, respectively, and is likely to achieve herd immunity in the first quarter of 2022, with unemployment at the end of 2022 at 2.7 million.

- If the government can distribute only 64.4 million doses, it will result in only 1.5% GDP growth in 2021 and 2.8% in 2022. In this case, the total GDP for 2021-2022 will be 3% (460 billion baht) lower than the scenario where 100 million doses are distributed, and the number of foreign tourists will drop to 1 million in 2021 and 12 million in 2022, with herd immunity likely delayed to the third quarter of 2022, and unemployment at the end of 2022 at 2.8 million.

- If the government distributes fewer than 64.4 million doses in 2021, it will result in only 1% GDP growth in 2021 and 1.1% in 2022, with total GDP for 2021-2022 being 5.7% (890 billion baht) lower than the scenario where 100 million doses are distributed. Additionally, the number of foreign tourists will be 0.8 million in 2021 and 8 million in 2022, with herd immunity likely delayed to the fourth quarter of 2022, and unemployment at the end of 2022 reaching 2.9 million.

The BoT assesses that overall liquidity is at a high level and financial costs are low, but the distribution of liquidity remains uneven due to increased credit risks. Therefore, it is necessary to monitor the more inclusive growth of credit after the implementation of the recovery credit measures. The yield on long-term Thai government bonds has decreased from previous periods. For the Thai baht against the U.S. dollar, it has weakened compared to regional currencies. The committee recommends closely monitoring developments in global and Thai financial markets, as well as continuously promoting the creation of a new FX ecosystem.

The BoT states that the continuity of government measures and policy coordination among agencies is crucial for the economic recovery from the new outbreak. Measures to procure and distribute vaccines should be accelerated to prevent prolonged outbreaks. Fiscal measures should maintain the continuity of fiscal stimulus and reduce the impact of the outbreak, as well as support the economic recovery in the future. Monetary policy must remain accommodative. Additional assistance measures for businesses affected by the COVID-19 outbreak should be expedited to distribute liquidity to affected parties effectively, reduce debt burdens, and support future economic recovery, alongside pushing financial institutions to accelerate debt restructuring for borrowers. The BoT will closely monitor the progress and evaluate the effectiveness of financial and credit measures.

The BoT continues to emphasize supporting economic recovery as a priority within the framework of monetary policy aimed at maintaining price stability while ensuring sustainable and full economic growth and financial system stability. Additionally, the BoT will monitor key factors affecting economic trends, including the new outbreak situation, vaccine distribution and effectiveness, and the adequacy of already implemented fiscal and monetary measures, ready to utilize appropriate monetary policy tools if necessary.

Implications

EIC expects the BoT to maintain the policy interest rate at 0.5% throughout 2021 and will prioritize measures to distribute liquidity to affected businesses and support debt restructuring. The BoT is likely to keep the policy interest rate at this level to support economic recovery, especially as the economy is impacted by the new outbreak of COVID-19, which EIC views as having a low chance of further reducing the policy interest rate.

- The transmission of monetary policy may face more limitations when interest rates are very low, as further reducing the policy interest rate may not significantly stimulate demand in the economy due to reduced purchasing power and consumer confidence, which relies on interest income from deposits that may decline with lower deposit rates, thus affecting consumption trends. Additionally, stimulating investment may not be feasible in a high-uncertainty environment.

· Reducing the policy interest rate may help lower financial costs somewhat, but it does not play a role in distributing liquidity to businesses and households with high credit risks. Therefore, the critical issue of access to funding sources for those affected by the outbreak remains.

· The declining deposit interest rates approaching zero may lead to the accumulation of vulnerabilities in the financial sector due to search-for-yield behavior that results in underestimating investment risks, particularly among savers who still lack adequate financial literacy.

Therefore, EIC assesses that the BoT will focus on enhancing the efficiency of measures supporting business loans and asset warehousing measures (or "debt and asset relief measures") that have been implemented, and may extend the measures to reduce contributions to the Financial Institutions Development Fund (FIDF). Recently, the BoT has adjusted the conditions of the previous soft loan measures to cover the target groups affected and provide more operational flexibility. Additionally, the BoT may extend the period for reducing contributions to the FIDF from the previously announced rate of 0.23% for a duration of 2 years (from the announcement date in April 2020).

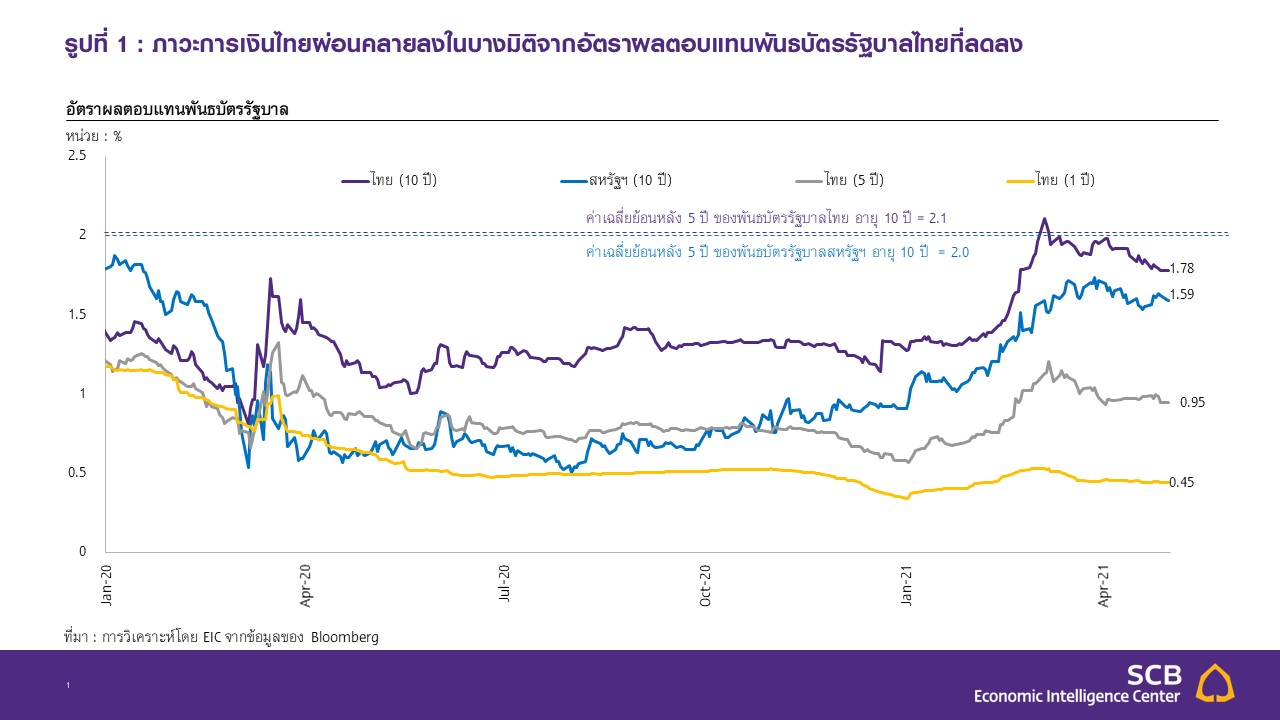

The financial situation in Thailand has eased in some dimensions, as the yield on Thai government bonds has decreased in recent months in line with the decline in U.S. government bond yields. Currently, the yield on 10-year Thai government bonds is at 1.78%, down 19 bps since early April, while the yield on 10-year U.S. government bonds is at 1.59%, down 14 bps during the same period (Figure 1).

- The yield on U.S. government bonds decreased in April 2021, which does not align with the economic data from the U.S., including non-farm payrolls and the producer price index, which have continuously risen, indicating a strong economic recovery. The decline in U.S. government bond yields stems from three main factors:

- Market participants have anticipated a trend of reducing the Fed's monetary policy easing, with most assessing that the Fed will begin raising the policy interest rate for the first time in the first quarter of 2023, earlier than the Fed communicated for 2024. This reflects that market participants expect the U.S. economy to grow rapidly, potentially pressuring the Fed to raise interest rates sooner than communicated. Therefore, even though U.S. economic data continues to be positive, the market has already anticipated this, leading to no significant increase in U.S. government bond yields.

- Investors have adjusted their positive outlook on U.S. economic growth and inflation in the medium and long term due to geopolitical tensions and the suspension of the Johnson & Johnson vaccine. Additionally, investors view that short-term inflation in the U.S. is likely to rise faster than medium- and long-term inflation, resulting in a decline in long-term U.S. government bond yields.

- The purchase of U.S. government bonds by foreign investors in early April, as reported by the U.S. Treasury, indicated that Japanese investors purchased U.S. government bonds in the second week of April 2021, primarily from pension funds, resulting in a decrease in U.S. government bond yields due to increased demand.

- The yield on Thai government bonds has decreased in line with the trend of declining U.S. government bond yields, the Thai economy is showing signs of significant slowdown, and the number of COVID-19 cases continues to rise from the third wave, coupled with slow vaccine distribution, leading to a slower-than-expected growth outlook for the Thai economy, which has pressured the yield on Thai government bonds to decrease.

Figure 1: Thai Financial Conditions Eased in Some Dimensions from Decreased Yields on Thai Government Bonds

Source: Analysis by EIC from Bloomberg data

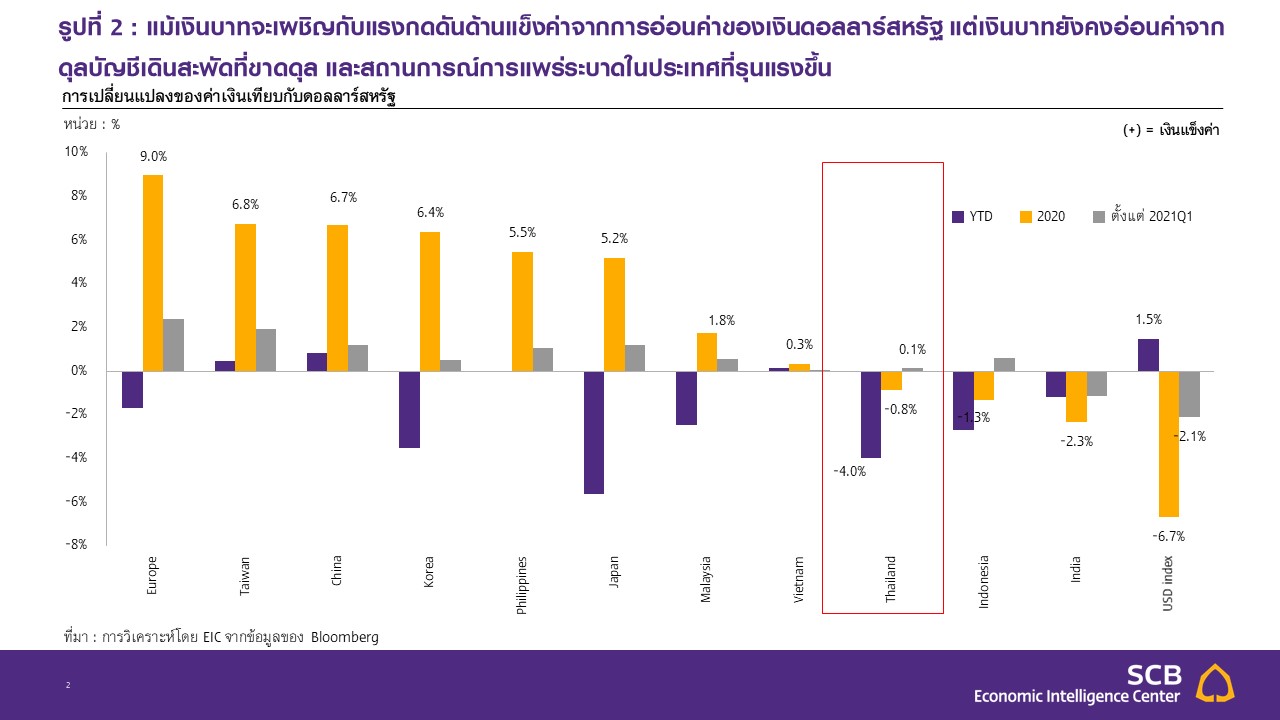

Although the U.S. dollar has weakened, the Thai baht has depreciated against regional currencies due to a current account deficit and worsening domestic outbreak situations. Currently, the baht stands at 31.2 baht per U.S. dollar, depreciating 4% since the beginning of the year, which is a greater depreciation than other regional currencies. Compared to the previous quarter, the baht remains stable even though the U.S. dollar index has weakened by -2.1% during the same period (Figure 2). The factors causing the baht to weaken include:

- The current account deficit of Thailand since the beginning of the year, with a total deficit of 77 billion baht in the first quarter, the lowest level since 2013, primarily due to a -99.7% year-on-year contraction in foreign tourist numbers in the first quarter. Additionally, while exports grew by 0.2% year-on-year in the first quarter, imports grew by 7.2% year-on-year, resulting in a trade deficit of 12 billion baht in the first quarter.

- The worsening domestic outbreak situation, coupled with slow vaccine rollout progress, has affected investor confidence, causing capital flows into Thailand to remain sluggish. Although there has been capital inflow into the bond market in 2021, there has also been capital outflow from the Thai stock market at levels close to those entering the bond market.

Figure 2: Despite the Baht Facing Appreciation Pressure from the Weaker U.S. Dollar, the Baht Continues to Depreciate Due to Current Account Deficit and Worsening Domestic Outbreak Situations

Source: Analysis by EIC from Bloomberg data

Analysis from EIC website…https://www.scbeic.com/th/detail/product/7556